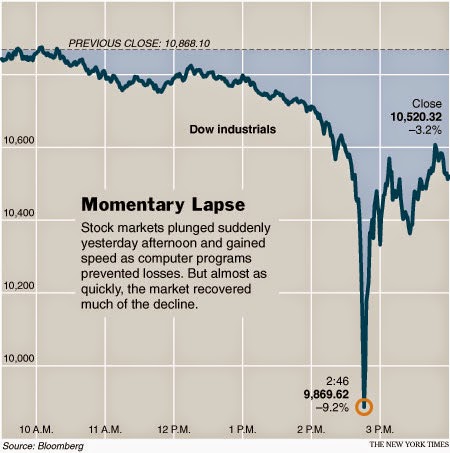

Early in the afternoon of 6 May 2010, the leading stock market index in the US, the Dow Jones Industrial Average, suddenly started falling. There was no evident external reason for the fall – no piece of news or economic data – but the market, which had been drifting slowly downwards that day, in a matter of minutes dropped by 6 per cent. There was pandemonium: some stocks in the Dow were trading for prices as low as 1 cent, others for prices as high as $100,000, in both cases with no apparent rationale. A 15-minute period saw a loss of roughly $1 trillion in market capitalisation.

So far, so weird, but it wasn’t as if nothing like this had ever happened before. Strange things happen in markets, often with no obvious trigger other than mass hysteria; there’s a good reason one of the best books about the history of finance is called Manias, Panics and Crashes. What was truly bizarre and unprecedented, though, was what happened next. Just as quickly as the market had collapsed, it recovered. Prices bounced back, and at the end of a twenty-minute freak-out, the Dow was back where it began. It’s the end of the world! Oh wait, no, it’s just a perfectly normal Thursday.

This incident became known as the Flash Crash. The official report from the Securities and Exchange Commission blamed a single badly timed and unhelpfully large stock sale for the crash, but that explanation failed to convince informed observers. Instead, many students of the market blamed a new set of financial techniques and technologies, collectively known as high-frequency trading or flash trading. This argument rumbles on, and attribution of responsibility is still hotly contested. The conclusion, which becomes more troubling the more you think about it, is that nobody entirely understands the Flash Crash.

This incident became known as the Flash Crash. The official report from the Securities and Exchange Commission blamed a single badly timed and unhelpfully large stock sale for the crash, but that explanation failed to convince informed observers. Instead, many students of the market blamed a new set of financial techniques and technologies, collectively known as high-frequency trading or flash trading. This argument rumbles on, and attribution of responsibility is still hotly contested. The conclusion, which becomes more troubling the more you think about it, is that nobody entirely understands the Flash Crash.

The Flash Crash was the first moment in the spotlight for high-frequency trading. This new type of market activity had grown to such a degree that most share markets were now composed not of humans buying and selling from one another, but of computers trading with no human involvement other than in the design of their algorithms. By 2008, 65 per cent of trading on public stock markets in the US was of this type. Actual humans buying and selling made up only a third of the market. Computers were (and are) trading shares in thousandths of a second, exploiting tiny discrepancies in price to make a guaranteed profit. Beyond that, though, hardly anybody knew any further details – or rather, the only people who did were the people who were making money from it, who had every incentive to keep their mouths shut. The Flash Crash dramatised the fact that public equity markets, whose whole rationale is to be open and transparent, had arrived at a point where most of their activity was secret and mysterious.

Enter Michael Lewis. Flash Boys is a number of things, one of the most important being an exposition of exactly what is going on in the stock market; it’s a one-stop shop for an explanation of high-frequency trading (hereafter, HFT). The book reads like a thriller, and indeed is organised as one, featuring a hero whose mission is to solve a mystery. The hero is a Canadian banker called Brad Katsuyama, and the mystery is, on the surface of it, a simple one. Katsuyama’s job involved buying and selling stocks. The problem was that when he sat at his computer and tried to buy a stock, its price would change at the very moment he clicked to execute the trade. The apparent market price was not actually available. He raised the issue with the computer people at his bank, who first tried to blame him, and then when he demonstrated the problem – they watched while he clicked ‘Enter’ and the price changed – went quiet.

Katsuyama came to realise that his problem was endemic across the financial industry. The price was not the price. The picture of the market given by stable prices moving across screens was an illusion; the real market was not available to him. Very many people across the industry must have asked themselves what the hell was going on, but what’s unusual about Katsuyama is that he didn’t let the question go: he kept going until he found an answer. Part of that answer came in correctly formulating the question, what the hell is the market anyway?

Image: Bloomberg

So far, so weird, but it wasn’t as if nothing like this had ever happened before. Strange things happen in markets, often with no obvious trigger other than mass hysteria; there’s a good reason one of the best books about the history of finance is called Manias, Panics and Crashes. What was truly bizarre and unprecedented, though, was what happened next. Just as quickly as the market had collapsed, it recovered. Prices bounced back, and at the end of a twenty-minute freak-out, the Dow was back where it began. It’s the end of the world! Oh wait, no, it’s just a perfectly normal Thursday.

This incident became known as the Flash Crash. The official report from the Securities and Exchange Commission blamed a single badly timed and unhelpfully large stock sale for the crash, but that explanation failed to convince informed observers. Instead, many students of the market blamed a new set of financial techniques and technologies, collectively known as high-frequency trading or flash trading. This argument rumbles on, and attribution of responsibility is still hotly contested. The conclusion, which becomes more troubling the more you think about it, is that nobody entirely understands the Flash Crash.The Flash Crash was the first moment in the spotlight for high-frequency trading. This new type of market activity had grown to such a degree that most share markets were now composed not of humans buying and selling from one another, but of computers trading with no human involvement other than in the design of their algorithms. By 2008, 65 per cent of trading on public stock markets in the US was of this type. Actual humans buying and selling made up only a third of the market. Computers were (and are) trading shares in thousandths of a second, exploiting tiny discrepancies in price to make a guaranteed profit. Beyond that, though, hardly anybody knew any further details – or rather, the only people who did were the people who were making money from it, who had every incentive to keep their mouths shut. The Flash Crash dramatised the fact that public equity markets, whose whole rationale is to be open and transparent, had arrived at a point where most of their activity was secret and mysterious.

Enter Michael Lewis. Flash Boys is a number of things, one of the most important being an exposition of exactly what is going on in the stock market; it’s a one-stop shop for an explanation of high-frequency trading (hereafter, HFT). The book reads like a thriller, and indeed is organised as one, featuring a hero whose mission is to solve a mystery. The hero is a Canadian banker called Brad Katsuyama, and the mystery is, on the surface of it, a simple one. Katsuyama’s job involved buying and selling stocks. The problem was that when he sat at his computer and tried to buy a stock, its price would change at the very moment he clicked to execute the trade. The apparent market price was not actually available. He raised the issue with the computer people at his bank, who first tried to blame him, and then when he demonstrated the problem – they watched while he clicked ‘Enter’ and the price changed – went quiet.

Katsuyama came to realise that his problem was endemic across the financial industry. The price was not the price. The picture of the market given by stable prices moving across screens was an illusion; the real market was not available to him. Very many people across the industry must have asked themselves what the hell was going on, but what’s unusual about Katsuyama is that he didn’t let the question go: he kept going until he found an answer. Part of that answer came in correctly formulating the question, what the hell is the market anyway?

The market was by now a pure abstraction. There was no obvious picture to replace the old one people carried around in their heads. The same old ticker tape ran across the bottom of television screens – even though it represented only a tiny fraction of the actual trading. Market experts still reported from the floor of the New York Stock Exchange, even though trading no longer happened there. For a market expert truly to get inside the New York Stock Exchange, he’d need to climb inside a tall black stack of computer servers locked inside a fortress guarded by a small army of heavily armed men and touchy German shepherds in Mahwah, New Jersey. If he wanted an overview of the stock market – or even the trading in a single company like IBM – he’d need to inspect the computer printouts from twelve other public exchanges scattered across northern New Jersey, plus records of the private deals that occurred inside the growing number of dark pools. If he tried to do this, he’d soon learn that there was no computer printout. At least no reliable one. It didn’t seem possible to form a mental picture of the new financial market.We want a market to be people buying and selling to and from each other, in a specific physical location, ideally with visible prices. In this new market, the principal actors are not human beings, but algorithms; the real action happens inside computers at the exchanges, and the old market is now nothing more than a stage set whose main function is to be a backdrop for news stories about the stock market. As for the prices, they move when you try to act on them, and anyway, as Lewis says, there’s the problem of the ‘dark pools’, which are in effect private stock markets, owned for the most part by big investment banks, whose entire function is to execute trades out of sight of the wider public: nobody knows who’s buying, nobody knows who’s selling, and nobody knows the prices paid. The man who did most to help Katsuyama understand this new market was an Irish telecoms engineer called Ronan Ryan. Ryan’s job involves the wiring inside stock exchanges, and he explained to Katsuyama just how crucial speed has become to the process of trading. All the exchanges now allow ‘co-location’, in which private firms install their own computer equipment alongside the exchanges’ own computers, in order to benefit from the tiny advantage this proximity gives in trading time.

As Ryan spoke, he filled huge empty spaces on Brad’s mental map of the financial markets. ‘What he said told me that we needed to care about microseconds and nanoseconds,’ said Brad. The US stock market was now a class system, rooted in speed, of haves and have-nots. The haves paid for nanoseconds; the have-nots had no idea that a nanosecond had value. The haves enjoyed a perfect view of the market; the have-nots never saw the market at all. What had once been the world’s most public, most democratic, financial market had become, in spirit, something like a private viewing of a stolen work of art.by John Lanchester, LRB | Read more:

Image: Bloomberg